This week, the total inventory of construction steel showed a divergence, with the total rebar inventory increasing by 0.42% WoW and the total wire rod inventory decreasing by 0.46% WoW. On the supply side, blast furnace steel mills are currently enjoying good profitability and relatively high production enthusiasm. However, influenced by expectations for production cuts driven by the "anti-rat race" policy and environmental protection-driven production restrictions in Tangshan and other regions, individual steel mills have cut production and undergone maintenance, leading to a decrease in construction material production. This week, the price increase of rebar in multiple regions was greater than that of steel scrap, improving the profitability of electric furnace steel mills. As a result, some electric furnace steel mills have extended their operating hours. On the demand side, with the continuation of high summer temperatures and increased precipitation, the progress of downstream construction has slowed down, making it difficult for demand to improve significantly. This week, the total rebar inventory changed from a decrease to an increase.

This week, the total rebar inventory stood at 5.121 million mt, increasing by 21,200 mt WoW, with a growth rate of 0.42% (previous value: -0.91%). Compared to the same period of the lunar calendar last year, it decreased by 1.9578 million mt, with a decline rate of 27.66% (previous value: -28.88%).

Table 1: Overview of Rebar Inventory

Data source: SMM

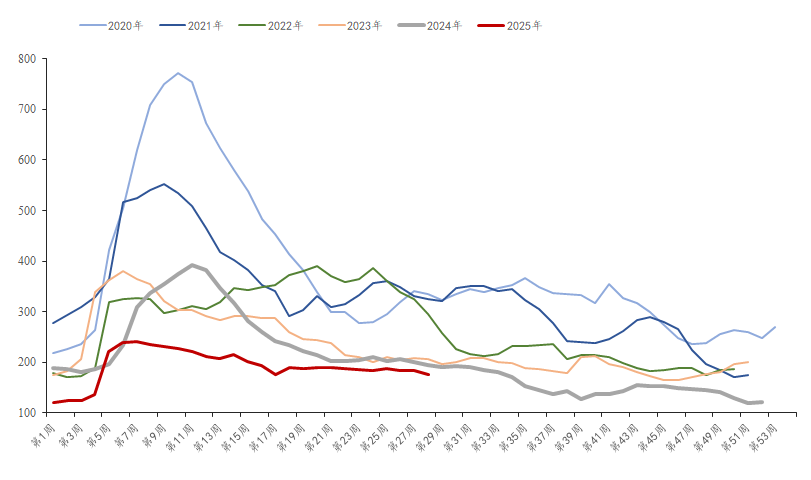

This week, the in-plant inventory of rebar was 1.7574 million mt, decreasing by 77,000 mt WoW, with a decline rate of 4.2% (previous value: +0.12%). Compared to the same period last year, it decreased by 177,200 mt, with a YoY decline of 9.16% (previous value: -4.3%). Currently, it is the traditional off-season for demand, and steel mills are facing increased supply pressure, leading to a decrease in production enthusiasm. Additionally, considering risk control, steel mills are accelerating the transfer of in-plant inventory to the market end, resulting in a decrease in construction material inventory at steel mills this week.

Chart-1: Overview of Rebar In-Plant Inventory Trends from 2020 to 2025

Data source: SMM

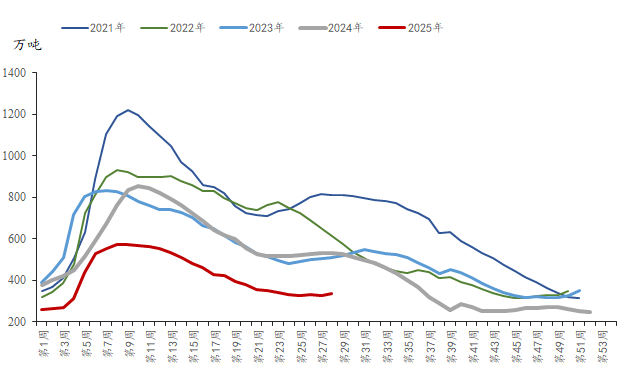

This week, the social inventory of rebar was 3.3636 million mt, increasing by 98,300 mt WoW, with a growth rate of 3.01% (previous value: -1.48%). Compared to the same period last year, it decreased by 1.7806 million mt, with a YoY decline of 34.61% (previous value: -37.85%). Recently, with the continuation of high temperatures, the actual demand from terminals remains suppressed by seasonal factors, and the trading volume of steel has decreased MoM. This week, the social inventory of rebar changed from a decrease to an increase.

Chart-2: Overview of Rebar Social Inventory Trends from 2021 to 2025

Data source: SMM

Overall, the current market is in the traditional off-season for the construction industry. High temperatures have slowed down construction progress at construction sites, and the demand for construction materials continues to be suppressed. Although steel mills have expectations for production cuts, considering the continuity of production and profit factors, the decline in steel production may be relatively limited. Therefore, it is expected that the total inventory of construction materials will accumulate next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)